Blog

Simple payroll, smart business

Tips, insights, and real small business experiences to help you run payroll with confidence (and maybe even enjoy it).

How the pros make payroll profitable: Peer insights

Discover how Canadian bookkeeping firms turn payroll into a profitable revenue stream. Get peer benchmarks on pricing, packaging, and scaling payroll for your firm.

Are labour insights hiding in your client’s chart of accounts?

Stop letting a generic chart of accounts hold your clients back. Learn how to turn payroll data into strategic advisory insights.

Hiring your first employee at a Canadian dental practice

Hiring your first employee is a turning point for any dental practice. Before you post the job, here’s what Canadian dentists need to know.

Your inside scoop on managing seasonal payroll in Canada

A practical guide to smooth payroll, happy employees, and stress-free summer operations.

Stop payroll scope creep: 5 habits of profitable accounting firms

Is unbilled payroll work hurting your margins? Discover 5 essential habits to stop scope creep and boost bookkeeping and accounting firm profitability.

Minimum wage by province 2026

Stay compliant by knowing the current minimum wage in your province or territory, plus when Canada’s federal minimum wage applies.

How Lime Bookkeeping turned payroll into their strongest retention tool

Before Wagepoint, payroll was costing Patrick 12 hours a day. Here’s what changed.

Introducing WagePAC: A strategic advisory council shaping the future of payroll.

We’ve always believed the best solutions are built with our partners, not just for them and their clients. That’s why we’re launching WagePAC — our first-ever Partner Advisory Council.

Managing a PIER report: Turn CRA reviews into client trust.

Managing a PIER doesn’t have to be stressful. Build client confidence by expertly guiding them and spotting advisory opportunities.

Everything you need to know about T4 amendments

Learn how to handle year-end T4 and T4A form amendments.

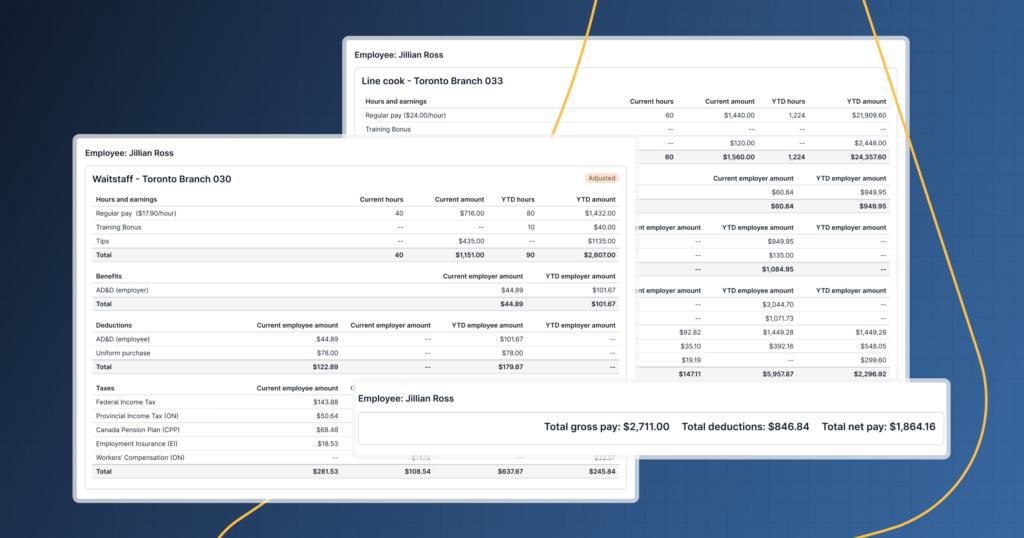

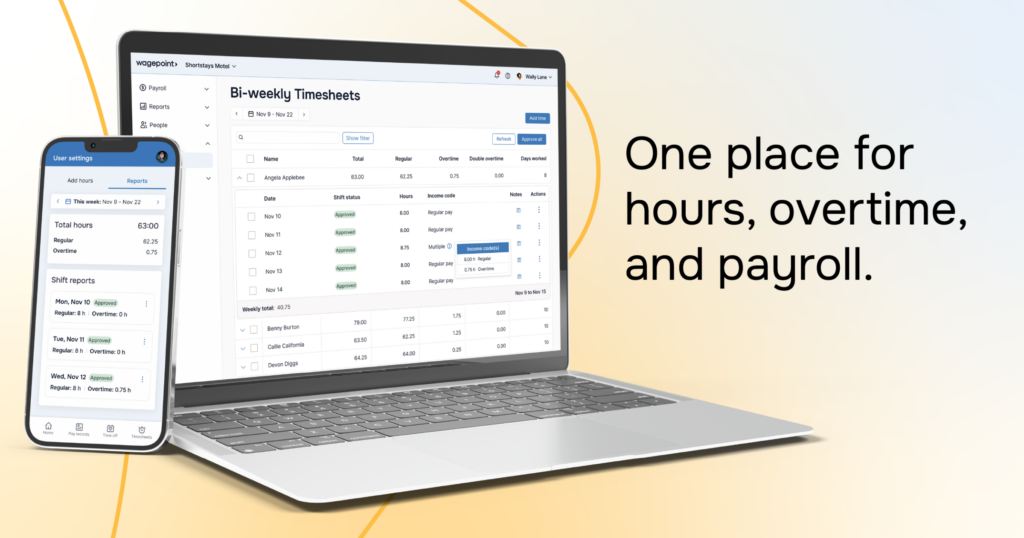

Timesheet chaos out. Stress-free payroll in.

Introducing Timesheets and the My Wagepoint mobile app. One connected system that brings time, pay, and mobile together.